Your Credit Score and How It’s Calculated

Whether you want to buy a car and take out an auto loan or borrow money from a lender to pay for school, a mortgage or any other big investment, one thing is for certain: your credit score determines your reliability. A decent credit score is the backbone to your financial wellness—it’s a reflection of your budgeting, spending and investing practices. Your credit score tells your bank or lender how big or little of a credit risk you are, but how exactly is a credit score calculated?

Whether you want to buy a car and take out an auto loan or borrow money from a lender to pay for school, a mortgage or any other big investment, one thing is for certain: your credit score determines your reliability. A decent credit score is the backbone to your financial wellness—it’s a reflection of your budgeting, spending and investing practices. Your credit score tells your bank or lender how big or little of a credit risk you are, but how exactly is a credit score calculated?

Credit Score Factors

There are several factors that go into your credits core. They are aptly called credit score factors. These include:

- Total debt

- Late payments

- Account types

- Age of accounts

The factors listed above combine together to make up your credit score. For example, if you have a lot of debt, it may not matter to some lenders as long as you’ve been repaying your debt responsibly. This is considered your payment history.

KEEP IN MIND: The higher balance you have in relation to your credit limit, the more this can affect your credit score. If you have $8,000 credit limit and you’re using $7,500 of it, this can negatively affect your credit score. Try to use at most 30% of your credit limit to keep your credit score in check.

In fact, more than 35% of your credit score is determined by how often you pay your bills on time and nothing else. If you need to improve your credit score, start with organizing all of your debt and paying a little more than the minimum payment, on time, every time.

How Your Credit Score is Calculated

Now, down to the formulaic nitty gritty. A credit score is a complex mathematical model that evaluates many types of information in a credit file to determine your financial reliability or credit risk; that is, how likely you are to repay a loan and make your loan payments on time.

The factors above influence your score, yet each factor affects your score differently.

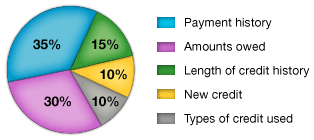

- As we mentioned above, 35% of your score is payment history (this includes payment information, bankruptcy, overdue payments, etc.),

- 30% is amounts owned (amounts owned on accounts individually and totaled together as a whole, accounts with balances and ratio of credit line used to credit line available).

- 15% is length of credit history (time since accounts have opened and how long they’ve been active)

- 10% is new credit (number of and time since recently opened accounts and proportion to total accounts, number of and time since recent credit inquires, and the re-establishment of positive credit history following past payment problems)

- 10% type of credit used (number of various types of accounts, like credit cards, retail accounts, installment loans, mortgage, etc.).

Since your credit score is a “snapshot”, it’s unlikely that your credit score a month ago is the same as it is today. Stay on top of your credit score and be sure to actively monitor your credit score. Credit scores change over time to accurately reflect your current financial behavior and length of credit history so the better your financial behavior, the better your credit score!